Introduction

Debt has become one of the most pressing financial challenges in modern life. From credit card balances and personal loans to student debt and medical bills, millions of households struggle every month just to keep up with minimum payments. The issue isn’t always due to insufficient earnings. More often, it is the absence of a clear, structured repayment plan.

When you are managing several debts at once, it can feel overwhelming. You are making payments to multiple lenders, watching interest pile up, and seeing very little visible progress. That sense of being stuck is one of the main reasons people give up on debt repayment far too early.

This is precisely where the Debt Snowball Method demonstrates its worth. It is a straightforward, psychologically powerful debt repayment strategy that helps you build momentum by targeting the smallest debt first. Paired with a debt snowball calculator, it becomes even more effective because you can see your exact payoff timeline and plan each month with confidence.

In this guide, you will find a complete explanation of how the debt snowball method works, a step-by-step breakdown, real-world examples, comparison with the debt avalanche method, and practical tips to help you get out of debt faster.

What is the Debt Snowball Method?

Debt Snowball Method Explained

The debt snowball method is a structured debt repayment strategy in which you focus all your extra financial energy on clearing the smallest debt first, while continuing to make minimum payments on all other debts. Once the smallest debt is fully paid off, you roll that freed-up payment amount into the next smallest debt. This process repeats until every debt is gone.

The term “snowball” is a reference to how a small snowball rolling downhill gradually picks up more snow and grows larger. Similarly, as each debt is cleared, your available payment amount grows bigger, and you pay off the remaining debts more and more quickly.

This method was widely popularized by personal finance author and radio host Dave Ramsey, who included it as a core step in his “Baby Steps” framework. However, the underlying logic of targeting small wins first has roots in behavioral economics and has been validated by multiple research studies on debt repayment behavior.

Unlike purely mathematical approaches to debt repayment, the debt snowball method prioritizes emotional momentum over interest rate optimization. This is intentional. The designers of this strategy recognized that human beings are more likely to stay consistent with a plan when they see and feel early progress.

Beginners in personal finance tend to prefer this method because it does not require complex calculations or a deep understanding of interest rates. The concept is simple, the steps are clear, and the results are visible relatively quickly.

How the Debt Snowball Method Works

The debt snowball method follows a clear five-step process. Here is a detailed breakdown of each stage.

Step 1: List All Your Debts

Begin by writing down every single debt you currently owe. This includes:

- Credit card balances

- Personal loans

- Student loans

- Medical bills

- Car loans or any other outstanding installment debt

Write down the total outstanding balance, the minimum monthly payment, and the interest rate for each one. Having this complete overview before you is a crucial starting point.

Step 2: Arrange Debts from Smallest to Largest Balance

Following that, arrange your debts from the lowest remaining balance to the highest. Disregard interest rates for now. The debt snowball strategy does not focus on which debt incurs the highest interest charges. It’s about determining which debt you can pay off first to build psychological momentum.chological momentum.

Seeing a debt completely wiped out is a powerful motivator. That small win keeps you committed to the process.

Step 3: Pay the Minimum on All Debts

Make the minimum required payment on every debt each month without exception. This keeps your accounts in good standing, protects your credit score, and ensures you do not incur penalty fees or damage your repayment history on other debts.

Step 4: Direct Extra Money Toward the Smallest Debt

Any additional money you can free up each month, whether from cutting discretionary expenses, a side income, a work bonus, or reduced spending, should go entirely toward the smallest debt. You are making a concentrated financial push to eliminate it as quickly as possible.

Even a modest extra payment of 50 to 100 dollars per month can dramatically reduce the time it takes to clear a small balance.

Step 5: Roll the Freed-Up Payment into the Next Debt

Once your smallest debt is paid off, do not increase your lifestyle spending with that freed-up money. Instead, roll the full amount you were paying on the eliminated debt directly into the next smallest debt on your list. Your payment amount just got bigger, and now you are attacking the next debt with more force.

This is the snowball effect in action. Each paid-off debt increases the payment power you bring to the next one, accelerating your overall debt-free timeline significantly.

Debt Snowball Example

To make this concrete, here is a practical example with three common debt types. Assume you have 200 dollars per month in extra funds available after minimum payments.

Debt Type | Outstanding Balance | Minimum Payment | Interest Rate |

Credit Card A | $500 | $50/month | 22% |

Personal Loan | $2,000 | $120/month | 14% |

Car Loan | $5,000 | $250/month | 9% |

Using the debt snowball method, you start by applying your extra $200 to the Credit Card A balance. So instead of paying $50, you are now paying $250 per month toward that $500 balance. It will be cleared in roughly two months.

After Credit Card A is gone, you roll that $250 into the personal loan. Now you are paying $370 per month toward that balance ($120 minimum plus $250 rolled over), clearing it far faster than the original schedule. Once the personal loan is eliminated, the full $370 gets added to the car loan payment, giving you $620 per month to drive that balance to zero.

The total monthly outflow remains the same. But the speed at which debts disappear accelerates dramatically with every elimination.

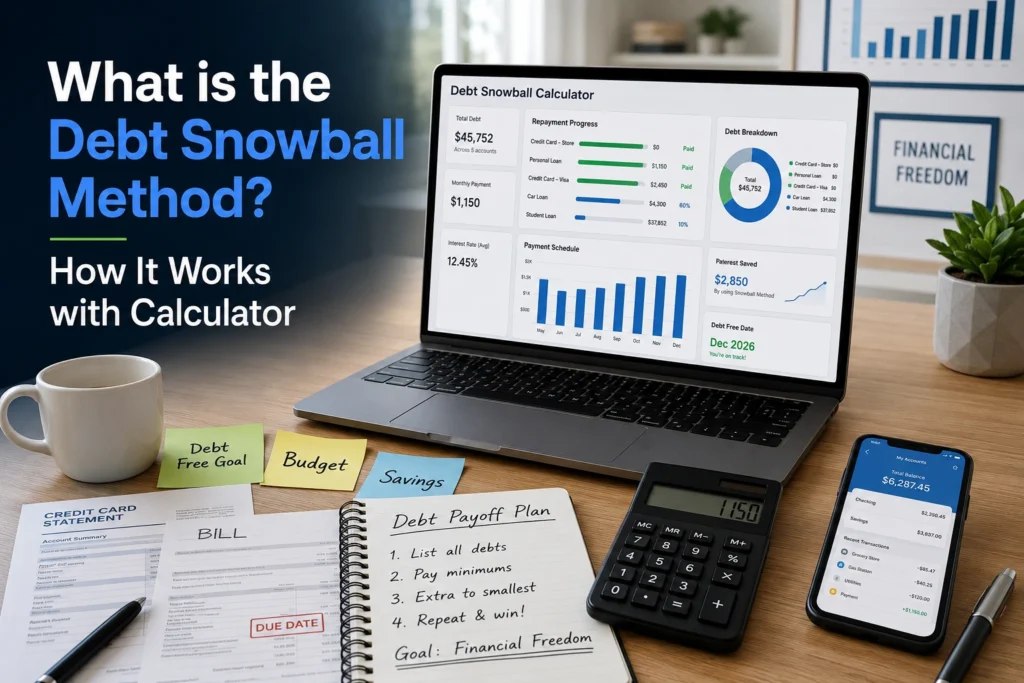

Debt Snowball Calculator: How It Helps

A debt snowball calculator is a digital tool that takes your debt information and computes a detailed repayment schedule automatically. Rather than manually working through the math each month, the calculator does the heavy lifting so you can focus on execution.

A good debt snowball calculator provides the following:

- A month-by-month repayment timeline for each debt

- Your estimated debt-free date

- Total interest paid across all debts

- A visual representation of your progress over time

- Comparisons of different extra payment scenarios

Information Needed in a Debt Snowball Calculator

To get accurate results, you will need to enter the following details for each debt:

- Total outstanding balance

- Current interest rate (APR)

- Required minimum monthly payment

- Any extra amount you plan to put toward debt each month

Once this data is entered, the calculator outputs a prioritized repayment order and a timeline showing exactly when each debt will be eliminated. Many free versions are available online, and some budgeting apps include built-in snowball calculators that update in real time as you log payments.

Benefits of the Debt Snowball Method

There are several reasons why the debt snowball method continues to be one of the most recommended debt repayment strategies for individuals at every income level.

- Builds motivation quickly through early small wins

- Extremely easy for beginners to understand and execute

- Creates disciplined money habits through consistent monthly action

- Reduces financial anxiety by showing tangible, measurable progress

- Encourages broader budgeting awareness and spending discipline

- Works well alongside other financial tools like emergency fund building

Drawbacks of the Debt Snowball Method

No single debt repayment strategy is perfect for every situation. The debt snowball method has a few notable limitations to be aware of.

- You may pay more total interest compared to methods that target high-interest debt first

- It can be slower in some cases than the debt avalanche method when large high-interest balances exist

- The method requires consistent financial discipline over months or years

These drawbacks do not outweigh the benefits for most beginners and average earners, but they are worth understanding before you commit to a plan.

Debt Snowball vs Debt Avalanche Method

The debt avalanche method is the main alternative to the debt snowball approach. Understanding the difference will help you choose the right strategy for your situation.

Key Differences

The debt avalanche method works by targeting the debt with the highest interest rate first, regardless of balance size. This approach minimizes the total interest paid over the life of your debt repayment journey. Mathematically, it is more efficient.

However, the debt snowball method prioritizes motivation and behavioral consistency. Research consistently shows that many people abandon financially optimal strategies if they do not see early progress. The debt snowball method addresses this psychological dimension directly.

Feature | Debt Snowball | Debt Avalanche |

Primary Focus | Smallest balance first | Highest interest rate first |

Motivation Level | High (early wins) | Moderate (slower visible progress) |

Total Interest Paid | Slightly higher | Lower (mathematically optimal) |

Best Suited For | Beginners, those needing motivation | Analytical planners, large high-rate debts |

Complexity | Low | Moderate |

If you are someone who thrives on visible progress and needs emotional reinforcement to stay committed, the debt snowball method is likely the better fit. If you have a high-interest debt like a credit card with a very large balance and strong financial discipline, the avalanche method may save you more money overall.

Tips to Make the Debt Snowball Method Work Faster

You can significantly speed up your debt-free timeline with a few practical strategies.

- Increase your extra monthly payment amount whenever possible, even by a small margin

- Review your monthly budget and identify subscriptions or habits you can temporarily cut

- Use a budgeting app to track every expense and find hidden savings opportunities

- Avoid taking on new debt while you are in active repayment mode

- Build a small emergency fund of at least one thousand dollars before beginning, so unexpected expenses do not derail your plan

- Track your debt balances monthly and celebrate every milestone, no matter how small

- Direct any windfalls such as tax refunds, work bonuses, or cash gifts entirely toward your current target debt

Common Mistakes to Avoid

Many people start strong with the debt snowball method but stumble due to avoidable errors. Here are the most frequent pitfalls to watch out for.

- Missing minimum payments on other debts while focusing on the target debt

- Taking on new debt during the repayment period, which undermines progress

- Treating freed-up payments as spending money instead of rolling them forward

- Failing to track debt balances and progress regularly

- Giving up during months when extra income is tight or progress feels slow

Consistency is the single most important ingredient. Even a modest but steady plan beats a perfect plan that gets abandoned.

Who Should Use the Debt Snowball Method?

The debt snowball method is not for everyone, but it is particularly well-suited for the following individuals.

- Beginners in personal finance who are just starting their debt-free journey

- People managing several smaller debts across multiple creditors

- Individuals who need visible early progress to stay motivated

- Families working together on a shared household debt repayment plan

- Anyone who has tried and abandoned other debt strategies due to slow visible results

Final Thoughts

The debt snowball method is one of the most proven and psychologically sound debt repayment strategies available. By targeting the smallest debt first and rolling freed-up payments forward, it creates a compounding momentum that accelerates your path to becoming completely debt-free.

It may not be the most mathematically optimal approach in every scenario, but for the majority of people, especially those new to structured financial planning, it works because it is built around human motivation rather than against it. Motivation and consistency will always outperform a technically superior plan that you abandon three months in.

Start by listing every debt you owe. Then use a free debt snowball calculator to map out your repayment timeline. Make your first extra payment this month, no matter how small. The journey to financial freedom begins with a single step, and the debt snowball method ensures each subsequent step gets easier and faster.

Frequently Asked Questions

Q 1: What is the debt snowball method in simple words?

The debt snowball method is a debt repayment strategy where you pay off your smallest debt first, while making minimum payments on all others. Once the smallest debt is eliminated, you redirect that payment to the next smallest debt and continue this pattern until all debts are fully paid.

Q 2: Is the debt snowball method effective?

Yes, it is highly effective for a large number of people. The primary reason is psychological. Clearing a small debt quickly delivers a sense of accomplishment that sustains motivation throughout the repayment journey. Studies in behavioral finance have confirmed that people are more likely to succeed with plans that offer early, visible rewards.

Q 3: Which is better: debt snowball or debt avalanche?

The debt avalanche method saves more money in interest over time, making it mathematically superior. However, the debt snowball method is better for most people because it keeps motivation high. If you have strong financial discipline and a large high-interest debt, the avalanche method may work better for your situation.

Q 4: How does a debt snowball calculator work?

A debt snowball calculator takes your debt balances, interest rates, minimum payments, and any extra monthly payment you can afford, then generates a complete repayment schedule. It tells you exactly when each debt will be paid off and provides an estimated date for when you will be completely debt-free.

Q 5: Can the debt snowball method improve your credit score?

Yes, it can have a positive effect on your credit score over time. Consistently making on-time payments, reducing outstanding balances, and eventually eliminating debts altogether all contribute to a healthier credit profile. Lowering your credit utilization ratio, especially on credit cards, typically produces a noticeable improvement in your credit score.

Q 6: What debts should be included in a debt snowball plan?

You can include most types of unsecured and secured personal debt, such as credit card balances, personal loans, medical bills, student loans, and car loans. Most financial advisors recommend excluding your primary mortgage from the snowball plan initially and focusing on consumer debt first. However, once all other debts are cleared, some people do apply the same rolling payment strategy to their mortgage.